Help your employees save for the future

RRSPs, TFSAs, VRSPs, PRPPs – when it comes to offering retirement savings plans to employees, there are lots to consider. Make it simpler for your employees to save for the future by helping them understand what their choices are.

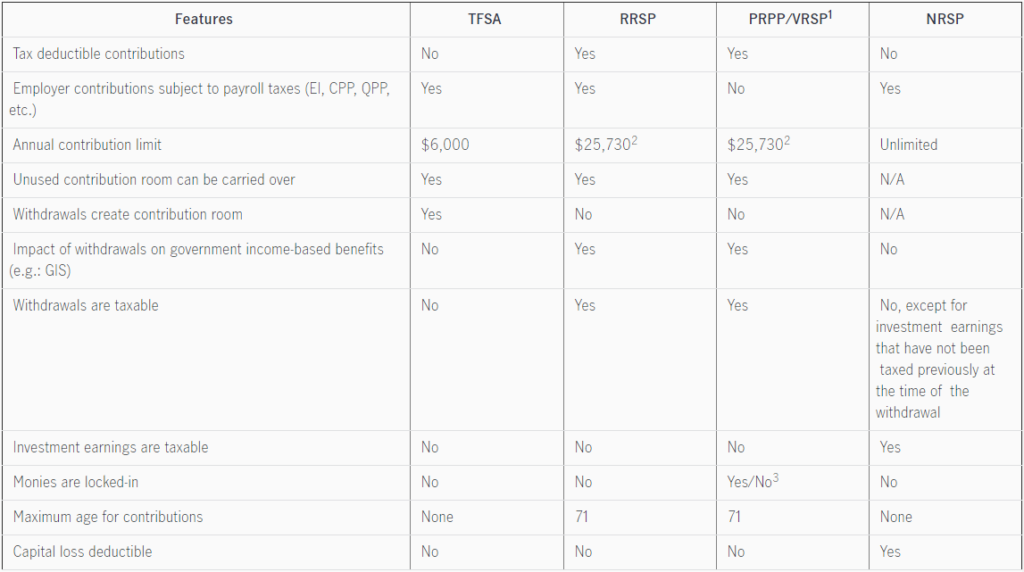

Use these short descriptions of savings plans and comparison chart so your employees can better understand the main benefits and differences between each option:

TFSA — Tax-Free Savings Account. Employee deposits into this type of account are made with after-tax income, therefore, the contributions and the investment earnings are not subject to tax. There is a limit to how much they can deposit in a TFSA.

RRSP — Registered Retirement Savings Plan. The money employees put into an RRSP and the interest earned are both subject to tax — but only on the date they’re withdrawn. The contribution limit is higher when compared to a TFSA.

PRPP — Pooled Registered Pension Plan. These plans are often preferred by small and medium-sized business, and by the self-employed. As with an RRSP, contributions are tax-deductible and subject to an annual limit.

VRSP — Voluntary Retirement Savings Plan. Offered only in Quebec, a VRSP is similar to a PRPP except that the employee’s contributions are not locked-in.

NRSP — Non-Registered Savings Plan. Your contributions are after-tax money, so they’re not taxed nor are they tax-deductible. Interest earned is taxed. There is no annual contribution limit.

A side-by-side comparison

Get advice

To find out which combination of plans will help your employees become better prepared for retirement, you’ll need to weigh a variety of factors, including tax efficiency and plan flexibility for you and your employees. At this point, it’s a good idea to speak to an advisor.

Notes:

1. The PRPP is for employees and self-employed workers whose employment is federally regulated:

- The VRSP is for Quebec employees and self-employed workers

- PRPP laws have also been introduced in British Columbia, Alberta, Saskatchewan, Nova Scotia and Ontario, but they are not yet in effect

2. The 2016 yearly contribution limit under both the RRSP and the PRPP/VRSP is the lesser of 18% of your previous year’s earned income or $25,730.

3. For PRPP, both employer and employee contributions are locked-in. For VRSP, the employer contributions are locked-in but employee contributions are not.

*Content Courtesy of Manulife

Contact Me:

Arvin Jimenez

Life and Health Insurance Broker

604-626-8447 | arvin@arvinjimenez.com